TER PPh 21 in Indonesia: Current Rules Under Evaluation

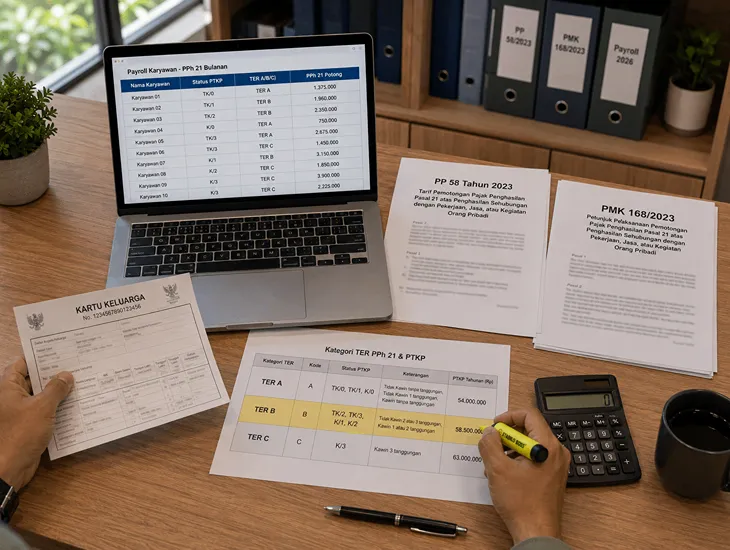

The legal basis is PP 58/2023. This regulation defines how employers withhold income tax. It provides the foundation for current payroll practices.

The legal basis is PP 58/2023. This regulation defines how employers withhold income tax. It provides the foundation for current payroll practices.

Implementation guidelines appear in PMK 168/2023. These rules detail the transition from old methods. Every business in Indonesia must follow them.

The system uses three main categories. These categories depend on the non-taxable income threshold. This threshold is known as PTKP in Indonesia.

Category A applies to single taxpayers without dependents. It also covers married individuals with no children. This group has the lowest threshold.

Category B includes taxpayers with one or two dependents. Most married employees with families fall here. The PTKP is higher than Category A.

Category C is for taxpayers with three dependents. This is the highest threshold for standard calculations. Accurate mapping prevents tax shortfalls.

Employers must verify the family status of workers. They should collect updated family cards and documents. This data ensures correct category selection.

Misclassification is a frequent error in Indonesian payroll. It causes incorrect tax amounts to be withheld. The tax office flags these inconsistencies.

The Directorate General of Taxes is currently evaluating the system. They want to ensure the effective rates work. This targets improvements for 2026.

The Directorate General of Taxes is currently evaluating the system. They want to ensure the effective rates work. This targets improvements for 2026.

Stakeholders provided feedback regarding the technical challenges. Some employers find system instability difficult. The tax office aims to simplify portals.

Vertical equity remains a topic of discussion. There are concerns about how rates affect non-regular income. Future adjustments may refine the bands.

Businesses must stay updated on these policy shifts. Rules valid in 2024 might change soon. The government issues circulars to clarify regulations.

Our firm monitors all announcements from the tax office. We provide clients with immediate updates on changes. This approach keeps your business compliant.

Interpretation differences lead to legal uncertainty. Different tax offices might view specific provisions differently. Expert guidance helps resolve these ambiguities.

Implementation costs were high for many companies initially. Updating software and training staff required resources. The goal is to reduce burdens.

The evaluation process ensures the system remains fair. It balances the needs of the government and taxpayers. Understanding trends helps in financial planning.