Resale Price Method in Indonesia: Understanding How It Works in Practice

Standing ministerial decrees explicitly define the acceptable methods used to apply the arm’s length principle. Local enforcement branches base their corporate reviews on updated transaction guidelines issued by the finance ministry.

Standing ministerial decrees explicitly define the acceptable methods used to apply the arm’s length principle. Local enforcement branches base their corporate reviews on updated transaction guidelines issued by the finance ministry.

Tax declarations must justify the choice of your selected valuation methodology through a comprehensive local file. Regulations mandate choosing the most appropriate method based on available internal and external market comparables.

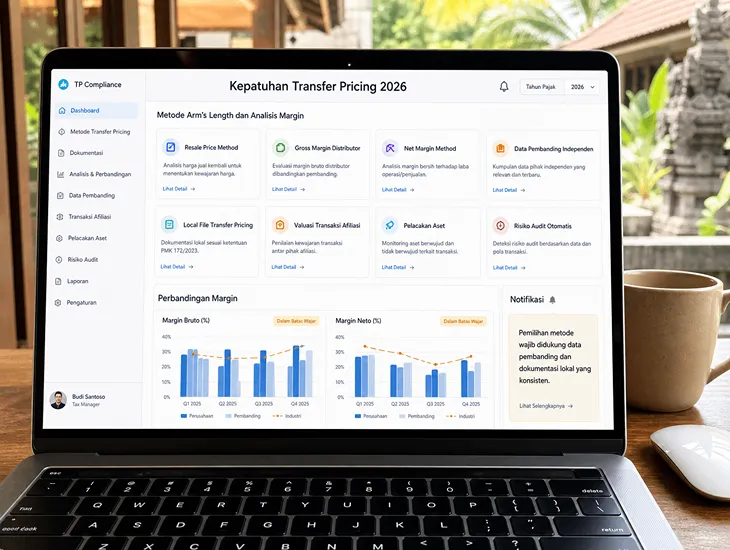

State decrees dictate that gross margin approaches remain optimal when independent distributor data is highly accessible. If reliable gross profit records are missing, examiners will push your enterprise toward net margin models.

Maintaining detailed asset tracking records ensures full compliance with localized transactional reporting mandates. Our advisory specialists align your annual corporate returns with active state directives to prevent automated data matching flags.

Staying updated on legislative transitions protects your international joint venture from unexpected tax collection demands. Structured financial accounting secures your investments against aggressive scrutiny from regional revenue enforcement boards.

Gross margin testing requires a high degree of functional comparability between the tested company and chosen market comparators. The underlying product lines do not need to be completely identical during the selection process.

Gross margin testing requires a high degree of functional comparability between the tested company and chosen market comparators. The underlying product lines do not need to be completely identical during the selection process.

Independent distributors operating within similar regional markets provide the most reliable baseline data for financial testing. Analysts must verify that these comparators share identical risk profiles regarding inventory obsolescence and customer default.

Resellers that own unique, valuable intangible assets or execute complex localized manufacturing cannot use this methodology. Owning proprietary brand trademarks or performing heavy product modifications fundamentally distorts gross profit tracking mechanisms.

Ensuring your distribution venture matches strict structural definitions guarantees long-term stability against sudden legislative changes. We filter through extensive regional databases to extract high-quality comparator profiles that withstand intensive state scrutiny.

Proper alignment of corporate parameters secures your financial records from arbitrary margin recomputations during audits. We establish stable accounting frameworks that allow your international trading business to expand safely across the country.