Foreign Investors in Indonesia: A Complete Guide to PT PMA

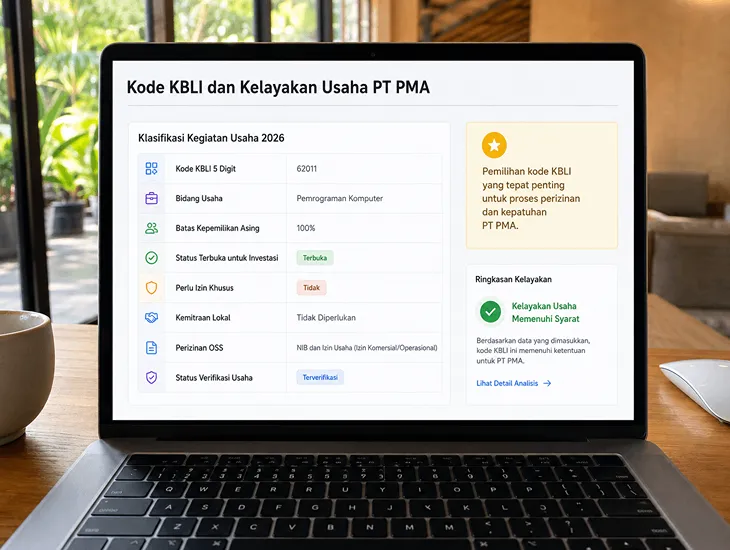

Commercial activities must map directly to standardized five-digit classification codes before initialization. These specific codes determine the maximum percentage of international equity permitted within your selected business sector.

Commercial activities must map directly to standardized five-digit classification codes before initialization. These specific codes determine the maximum percentage of international equity permitted within your selected business sector.

The state maintains a positive investment framework that keeps most commercial fields fully open to international capital. However, specific strategic sectors require local joint-venture partnerships or special ministerial permissions.

Selecting an incorrect classification code creates immediate friction during the licensing phase. Mismatched entries generate automatic systemic rejections, halting your corporate onboarding process across the central registration networks.

Investors must analyze these regulatory boundaries thoroughly before executing any official corporate deeds. Clear foresight prevents operational bottlenecks and ensures your business operations remain legally sound across all active provincial borders.

We guide your executive team through the complex business classification matrices to identify the exact code matches. Our meticulous verification process guarantees your enterprise secures the correct operational approvals efficiently.

Evolving investment rules demand ongoing tracking to catch sudden sector restrictions early. Keeping your structural records updated protects your ongoing licensing approvals from unexpected municipal interventions completely.

When Richard, a consumer logistics founder from Canada, first arrived in Pererenan, he struggled with complex corporate bookkeeping requirements for his regional setup. He faced an immediate administrative bottleneck while evaluating his multi-year corporate accounts.

When Richard, a consumer logistics founder from Canada, first arrived in Pererenan, he struggled with complex corporate bookkeeping requirements for his regional setup. He faced an immediate administrative bottleneck while evaluating his multi-year corporate accounts.

His internal accounting coordinators mistakenly assumed the preferential half-percent turnover tax rate would continue automatically into his fourth operational year without preparing standard financial statements. This created major hidden liabilities.

The newly launched digital tax platform detected this filing discrepancy immediately during a routine automated system cross-reference. The central database flagged his profile, initiating a comprehensive corporate tax audit.

This sudden tax dispute threatened his operational liquidity and severely disrupted his ongoing warehouse expansion plans. The technical error caused immense operational stress for his leadership team across the provinces.

He utilized a professional corporate advisory service to restructure his complete accounting history in accordance with state criteria. We compiled a verified reporting package and resolved his back-tax exposures within days.

Richard resumed his logistics operations under a fully monitored compliance schedule. This systematic alignment protected his consumer assets and secured his corporate longevity against future unforeseen institutional shocks.