PPh 21 DTP in Indonesia: Incentives for Labor-Intensive and Tourism Sectors

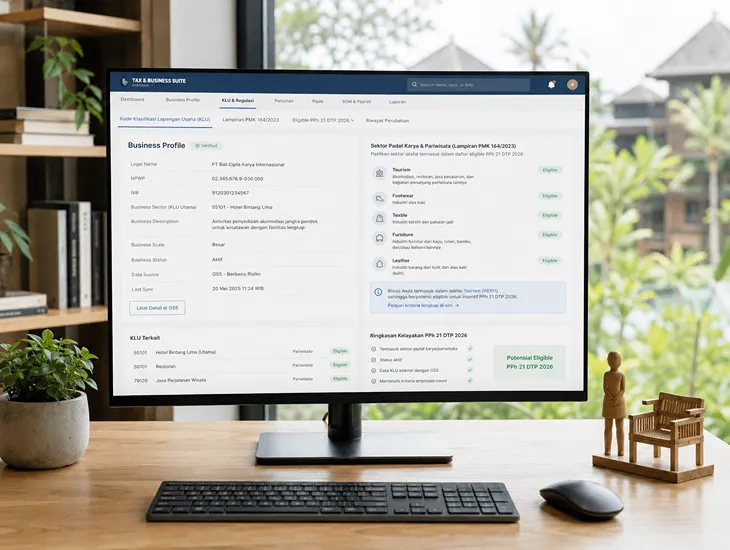

Eligibility depends heavily on your business classification. Only companies in labor-intensive or tourism sectors qualify. You must check your official Kode Klasifikasi Lapangan Usaha carefully. Footwear, textile, furniture, and leather industries are major beneficiaries.

Eligibility depends heavily on your business classification. Only companies in labor-intensive or tourism sectors qualify. You must check your official Kode Klasifikasi Lapangan Usaha carefully. Footwear, textile, furniture, and leather industries are major beneficiaries.

Tourism remains the backbone of the local economy in Bali. This sector includes travel agencies, hotels, and event organizers. You must verify your KLU code against Appendix A of PMK 105/2025 to secure benefits.

Many owners find their current KLU is outdated. Operating under the wrong code blocks access to this tax relief. You must synchronize your OSS data with national tax records immediately.

Proper classification prevents future disputes with the authorities. DGT officials use digital systems to verify industry codes instantly. We review your documents to ensure your digital profile reflects your actual business activities accurately.

Using the incentive requires submitting monthly realization reports. These digital files are uploaded via the DJP Online portal. You must meet the strict deadline of the 20th each month.

Using the incentive requires submitting monthly realization reports. These digital files are uploaded via the DJP Online portal. You must meet the strict deadline of the 20th each month.

The DJP Online portal is the central hub for all reporting. You must activate the specific e-Reporting service before your first submission. This one-time setup is crucial for your professional monthly workflow.

Preparation of the realization report requires specific file formats. The data must match your monthly tax return exactly. Inconsistencies will trigger official clarification letters from the regional tax office.

Missing the 20th deadline is a very common administrative mistake. This late filing can result in the complete loss of the incentive. We provide a rigorous calendar to keep your filings on track.

Uploading reports requires a stable internet connection and valid credentials. The portal can become busy near the monthly deadline. Filing early is a best practice to avoid unexpected technical connectivity issues.

You must also report the total number of eligible employees. DGT uses this data to track the distribution of the budget. Accuracy in these numbers is vital for maintaining your corporate tax reputation.

We handle the entire e-Reporting process for your business in Bali. Our team ensures that every submission is perfect and timely. We provide you with the receipt of realization for your internal records.